More Security Dollars and More Security Vendors

By combining our recent security trends survey and our core spending intentions survey, ETR examines how recent security trends might impact key players, such as SentinelOne, Zscaler, and Palo Alto. Let's take a closer look.

• The IT Security market landscape remains highly fragmented, but despite the belief that consolidation is inevitable, ETR's recent Security Trends Survey data suggests enterprises are increasing the total number of security vendors

• Combining responses with our latest TSIS indicates that larger platforms appear more poised to benefit from gaining net new customers

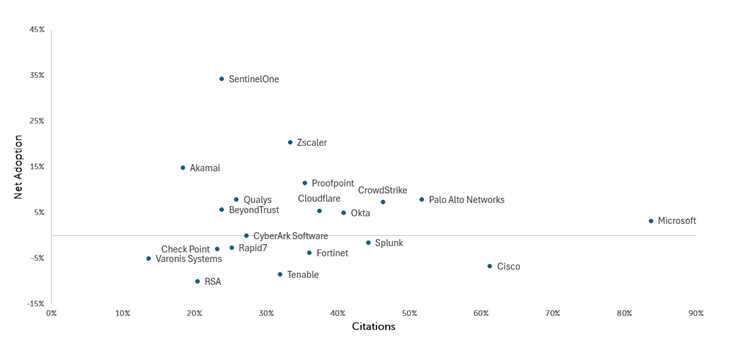

• Looking at net Adoption scores from the same respondents across surveys, SentinelOne, Zscaler, and Palo Alto Networks lead among these platforms

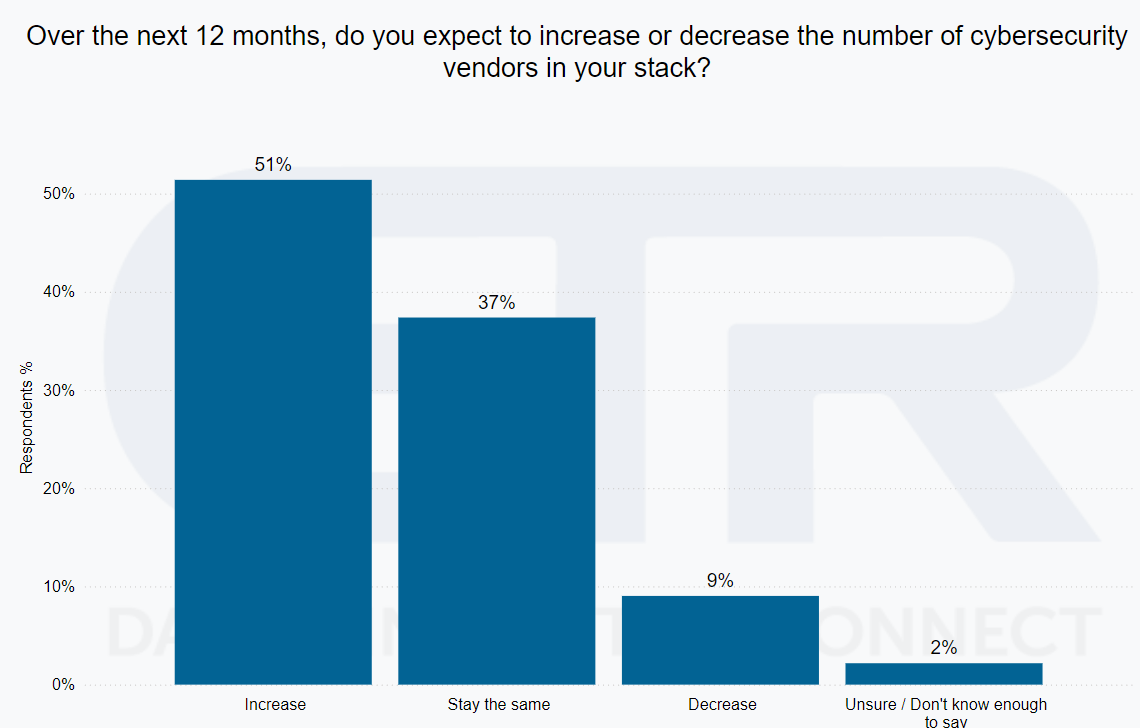

Enterprises are Increasing, Not Decreasing, InfoSec Vendors

The industry has watched as the higher growth, best-of-breed security vendors have built out their platforms over the past few years, moving well beyond their original core products. Several of these companies have cited feedback from customers looking to consolidate security into fewer vendors, arguing it comes with lower TCO, better tech integration, and reduced complexity for professionals using them. While these are beneficial to some enterprises, our recent Pre-RSA Security Trends survey data suggests a different trend: in the aggregate, enterprises are increasing the number of IT Security vendors.

With just over half of respondents indicating an expectation to increase the number of vendors, our data indicates that most enterprises are not eliminating vendors and shifting those functions to large platforms. Only 9% of respondents stated their intention to decrease their total vendor count, with consolidation the most popular reason (76%) for doing so, but we also find this is not unwelcome news for large platforms.

In fact, when we combine our Cybersecurity Drill Down data with respondents who also completed ETR's April 2024 Technology Spending Intentions Survey (TSIS) and filter for those intending to increase or keep flat total security spend, the results imply that larger security platforms seizing market share appear likeliest to benefit from total vendor increase. We see this across several categories of cybersecurity and note that SentinelOne, Zscaler, and Palo Alto Networks had particularly strong net Adoption scores (defined as percent of respondents intending to Adopt that vendor minus those intending to Replace).

Given the two most popular reasons for increasing vendors from our Cybersecurity Drill Down are for the ability to handle expected new threats and best-of-breed technology, we think platforms stand to benefit from a net new logo perspective. As they land these customers, we would expect the ongoing sales motion to drive account expansion and longer-term top line growth.

In the figure above, we isolate Aril 2024 TSIS respondents who indicated an increase in security vendors AND either Flat or Increasing budgets for this year. Among that segmented survey population, we plotted the Adoption / Replacement rates for security vendors (y-axis) and the overlapping citation percentage (x-axis).

SentinelOne Boasts the Highest Net Adoption Rate

The youngest of the three security providers we highlight has executed strong large account growth, with $100K+ ARR customers up 30% year over year (y/y) in the fourth quarter. The company has expanded beyond core endpoint products into data lake security, managed services, and cloud, closing its acquisition of PingSafe in February. (More on the PingSafe acquisition in ETR's upcoming Observatory Report on the Cloud Native Application Protection Platforms (CNAPP) report set to be published next week.)

ETR maintained a Positive Outlook on the company's data set in our April 2024 TSIS report, where SentinelOne saw the highest net Adoption percentage among all security vendors at 34%. The company was cited by 24% of respondents, which is modest compared to other platform vendors but reflects its status as a newer platform among companies with over half a billion dollars in ARR. However, it is rapidly gaining share and posted sales growth of 47% last fiscal year. SentinelOne competes well against other best-of-breed products and with the launch of its Singularity Data Lake product one year ago, appears well positioned to benefit from AI/ML data proliferation to drive logo growth.

Zscaler Solid Mix of High Adoptions and High Citations

Zscaler has continued to execute high growth, up 35% y/y in the latest quarter, with continued strength in $1M+ ARR accounts, which grew 30% y/y. In addition to large enterprises, we note a growing Net Score in SMBs according to our most recent TSIS data, which comprise most opportunities for potential new logos. For perspective, Zscaler counts over 40% of the Fortune 500 and over 30% of the Global 2000 as a customer.

Zscaler has invested in its product roadmap for Cloud and Network products while surpassing $2B in ARR. The company saw the second-highest net Adoption score among the half billion dollar-plus ARR vendors (excluding Microsoft) this quarter at 20% and was cited by 33% of ITDMs, which was well above the survey’s IT Security average of 19%. Anecdotal, qualitative feedback is also strong from numerous ETR Insights interviews.

Palo Alto Networks is Sticky But Net Adoption Lower

Palo Alto is highlighted due to its extremely low Replacement rate of 1% and impressive 52% citation level (second only to Microsoft of the 81 security vendors surveyed) in our most recent TSIS data set. More interestingly, the company sits at the heart of the platform debate and placed an attention-grabbing strategic bet on it last quarter. Palo Alto has built out dozens of products through development and frequent acquisitions, claiming that its Network, Cloud, and SOC platforms can each consolidate between 3-8 vendors. Although the company’s net Adoption score of 8% on our survey trails SentinelOne and Zscaler, the higher penetration (pervasion score) of the vendor may account for part of this difference, with fewer potential new customers to land given its relative maturity.

The company has favored platform consolidation for years but announced last quarter that it would offer its products free to customers switching from competitors while their existing contracts expire. With an estimated average free period of six months, Palo Alto is hoping to smooth the technical hurdles when switching critical IT systems, without cost to the customer. In connection with this, the company cut FY billings guidance by over 5% as it laid out the short-term impact on growth under its accelerated consolidation strategy. Despite a ubiquitous market presence, we think this strategic incentive and ability to compete across multiple segments positions the company well for first-time customers to Adopt new services as they reassess their vulnerabilities. The company also made news this week announcing its intent to purchase and leverage existing IBM security products, such as QRadar, which will likely grow an already entrenched customer base.

That's enough free data and analysis for one article, but if you would like to see more of what ETR has to offer, you can access our full research platform with a free trial.

Enterprise Technology Research (ETR) is a technology market research firm that leverages proprietary data from our targeted IT decision maker (ITDM) community to provide actionable insights about spending intentions and industry trends. Since 2010, we have worked diligently at achieving one goal: eliminating the need for opinions in enterprise research, which are often formed from incomplete, biased, and statistically insignificant data. Our community of ITDMs represents $1+ trillion in annual IT spend and is positioned to provide best-in-class customer/evaluator perspectives. ETR’s proprietary data and insights from this community empower institutional investors, technology companies, and ITDMs to navigate the complex enterprise technology landscape amid an expanding marketplace. Discover what ETR can do for you at www.etr.ai