Following our two-part series reviewing the Macro Views Survey data, this week, we dive into a high-level overview of the recently concluded July 2023 Technology Spending Intentions Survey (TSIS), ETR's core syndicated survey that has been conducted quarterly for more than 12 years. This data set is the original foundation on which ETR was built, and in this article, we will examine the high-level stats, sector-level trends, and overall vendor leaders and laggards that came out of this survey period.

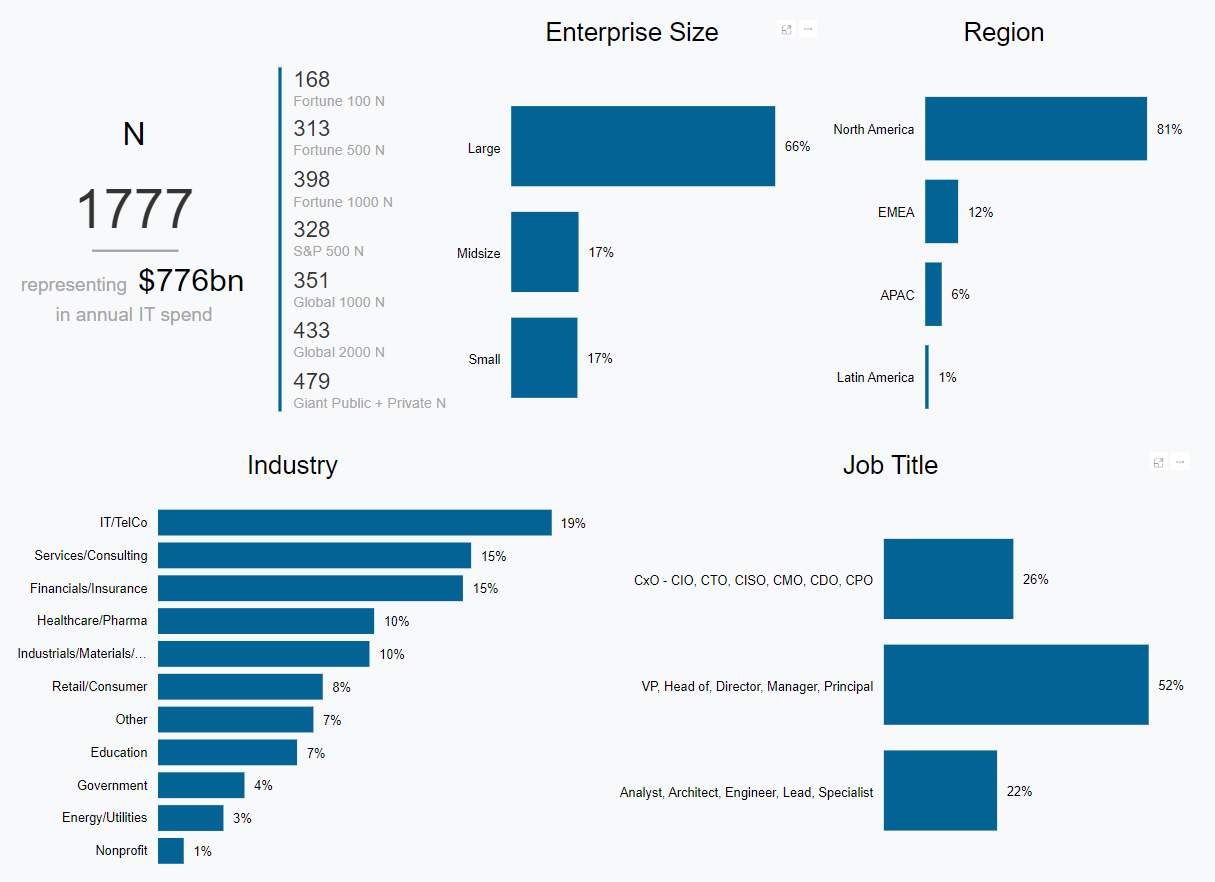

Let's begin with the statistics and demographics around the survey itself. The July 2023 iteration of the TSIS collected data from June 6th to July 7th and saw participation from nearly 1,800 IT Decision-Makers within ETR's community, including 313 Fortune 500 and 433 Global 2000 organizations. Of the total survey respondents, 26% hold C-suite titles, with another 52% respondents at the VP / Director level. By industry, IT/TelCo, Services/Consulting, and Financials/Insurance are the three most represented verticals, collectively accounting for 49% of respondents. Regarding enterprise size, 66% of respondents are from Large organizations, and 34% are from Mid & Small organizations.

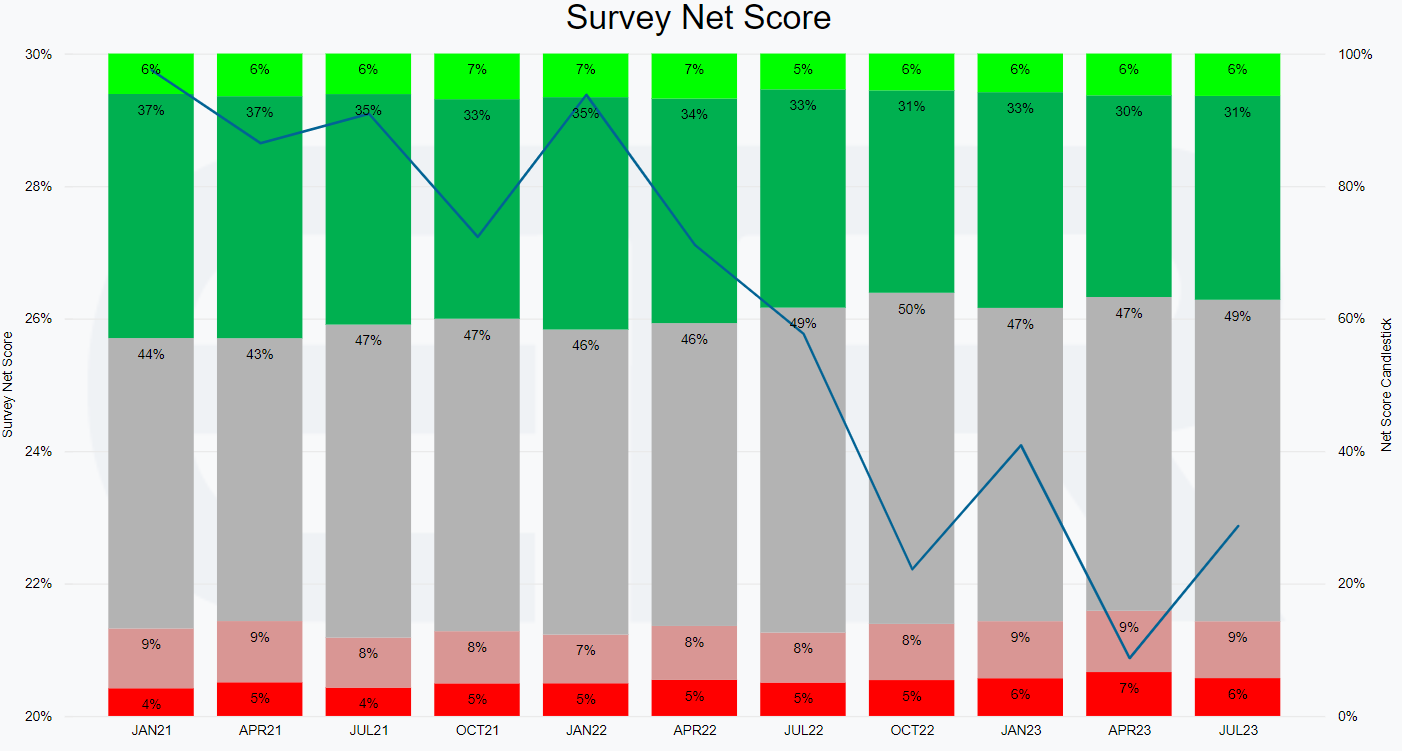

Now that we know the population that comprises our survey, let's take a look at the overall survey-level performance. While overall spending remains far below levels seen in 2021 and early 2022, this survey does reflect a sequential improvement since April 2023, with average Net Score landing slightly above October 2022 levels, as seen below. In the most recent quarter, survey-wide Net Score has landed at 23%, a 2 percentage-point improvement over last survey but still down considerably from early 2021 levels of 33%.

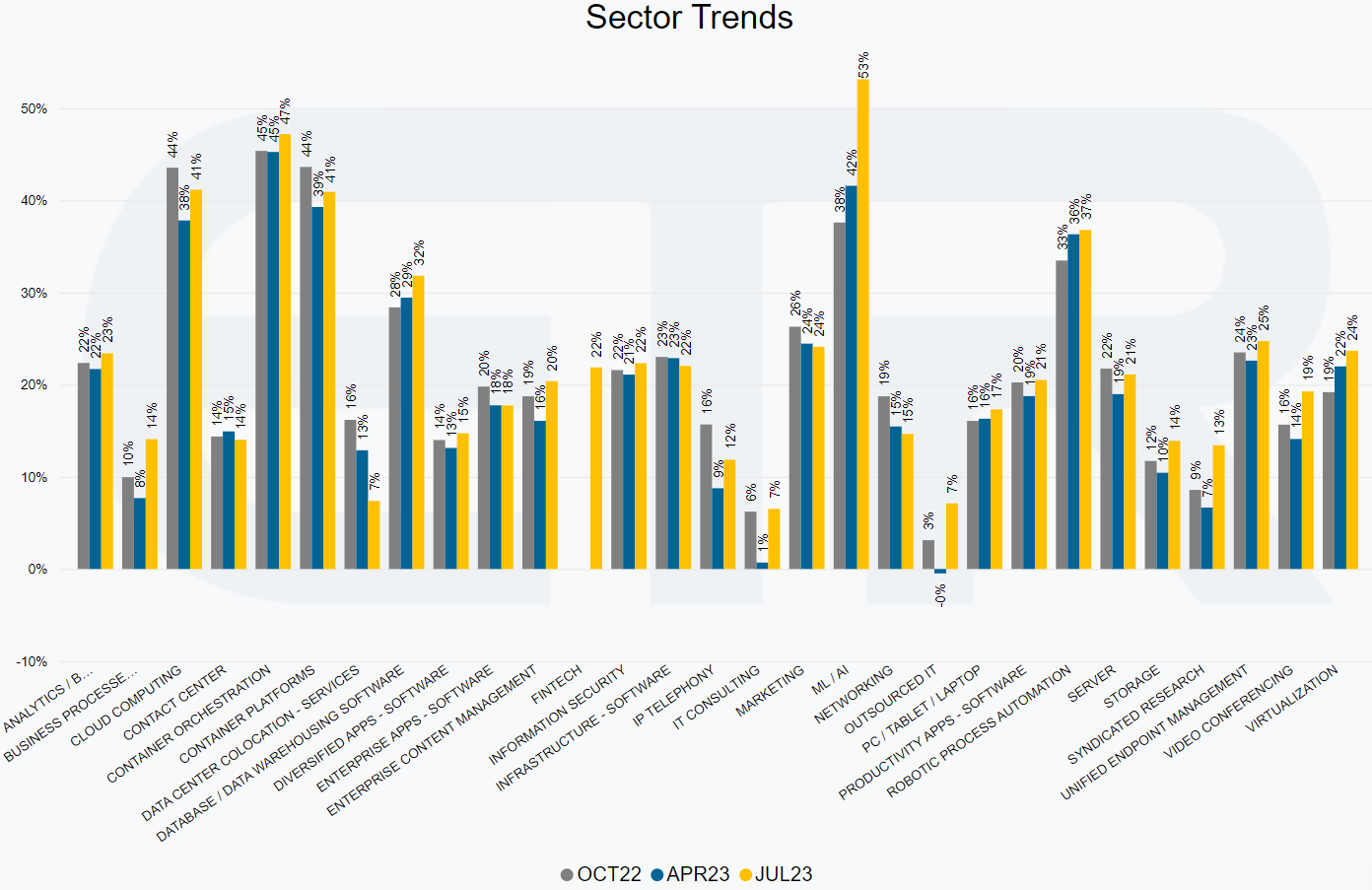

Next, we take a look at the sector-level trends, as depicted by the chart below. Here we view all technology sectors that ETR tracks ranked by their Net Scores, a measure that tracks positive spending rates on a forward-looking basis. After three survey periods of holding the highest sector Net Score, the Container Orchestration sector still saw a 2 percentage-point bump, though it was surpassed by the ML/AI sector which shows impressive survey-over-survey growth, improving from 42% in April 2023 to 53%. Third place remains a tie between the Cloud Computing and Container Platforms sectors with Net Scores of 41% each. Robotics Process Automation (RPA) rounds out the top 5 with a 37% Net Score for the sector.

Inversely, Outsourced IT, IT Consulting, and Data Center Colocation sectors are tied for the bottom spot, each registering a Net Score of 7%. While this represents a sequential improvement in spending intentions for the IT Consulting and Outsourced IT sectors, the Data Center Colocation sector has seen its Net Score drop incrementally since October 2022.

After reviewing the survey-wide and sector-level trends, ETR digs deeper into the individual vendor-level performance of the more than 400+ public companies tracked in the TSIS. The ETR platform has way too many data visualization and analysis models to touch upon in this article, but if you would like to see them all for yourself, you can gain access with a 100% free trial whenever you're ready.

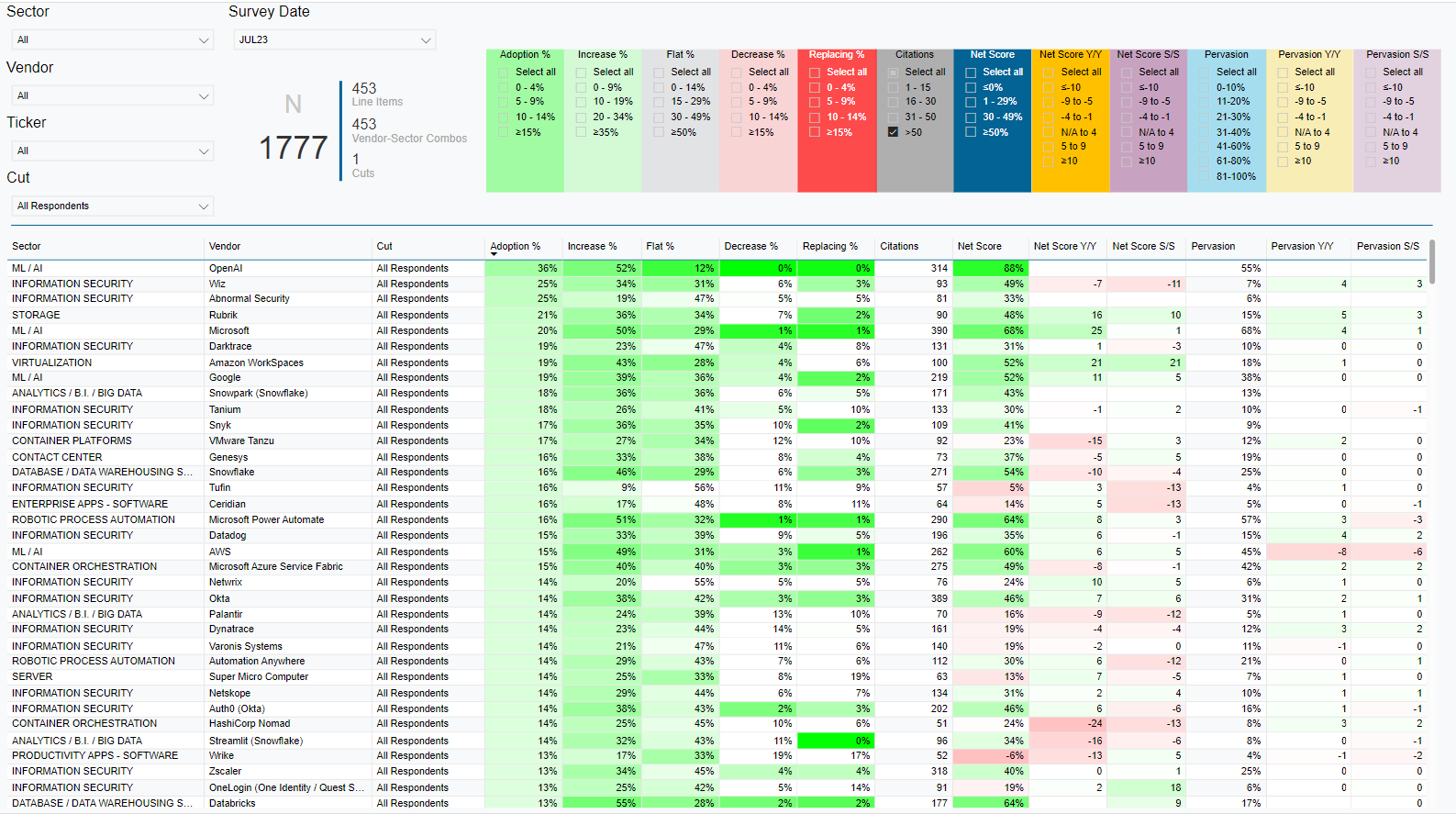

In the meantime, we will highlight one of the fastest and easiest ways to compare vendor-level data, which is by using our proprietary custom data filtering model. This model sorts the entire vendor universe by every answer option, metric, and respondent cut that ETR allows. The permutations are seemingly endless, so here we chose one metric as an example.

The image below ranks all vendors by Adoption rates and shows that all the buzz around OpenAI is translating to actual enterprise expenditure. The ML/AI vendor leads all vendors (with at least 50 citations) in Adoption rates, with a breathtaking 36% of its unique survey respondents citing plans to adopt the vendor (which incidentally has contributed to the material gain in spending seen within the ML/AI sector). At a quick glance, we can see that Increase spending on the vendor is even more impressive, at 52%, and that no respondents, at this point in the game, indicated negative intent on OpenAI. However, Microsoft's own metrics within the ML/AI are nothing to scoff at, with the 5th highest Adoption rates in the survey, at 20%, and a 50% Increase spending rate. Beyond ML/AI, we can also see that Wiz and Abnormal Security register the second best Adoption rates, coming in at 25%. Overall, ML/AI and Information Security vendors are well-represented sectors in this analysis with strong Adoptions.

Following each TSIS survey, the ETR Analytics & Research team reviews the entire survey-wide data sets to create sector- and vendor-level reports, including the highest conviction data sets for the best (and worst) performing vendors. Since that information is reserved for ETR Community members and clients, we will not be delving into those topics in this article; however, all of those reports, along with the 12 years of historical data, and visualization models, are available within the ETR Platform. If you would like to check it out, get started today, or reach out to us at service@etr.ai to schedule a demo.

Enterprise Technology Research (ETR) is a technology market research firm that leverages proprietary data from our targeted IT decision maker (ITDM) community to provide actionable insights about spending intentions and industry trends. Since 2010, we have worked diligently at achieving one goal: eliminating the need for opinions in enterprise research, which are often formed from incomplete, biased, and statistically insignificant data. Our community of ITDMs represents $1+ trillion in annual IT spend and is positioned to provide best-in-class customer/evaluator perspectives. ETR’s proprietary data and insights from this community empower institutional investors, technology companies, and ITDMs to navigate the complex enterprise technology landscape amid an expanding marketplace. Discover what ETR can do for you at www.etr.ai