Once again, the earnings calendar is packed with many tech companies that ETR tracks in our quarterly Technology Spending Intentions Survey (TSIS) reporting over the next two weeks, such as Zoom, CrowdStrike, Salesforce, Elastic, Workday, and others. In advance of the earnings reports, ETR has compiled some recent data on a handful of those companies. Remember the full data sets and reports are all available on the ETR platform. First up, we take a deep dive into Datadog.

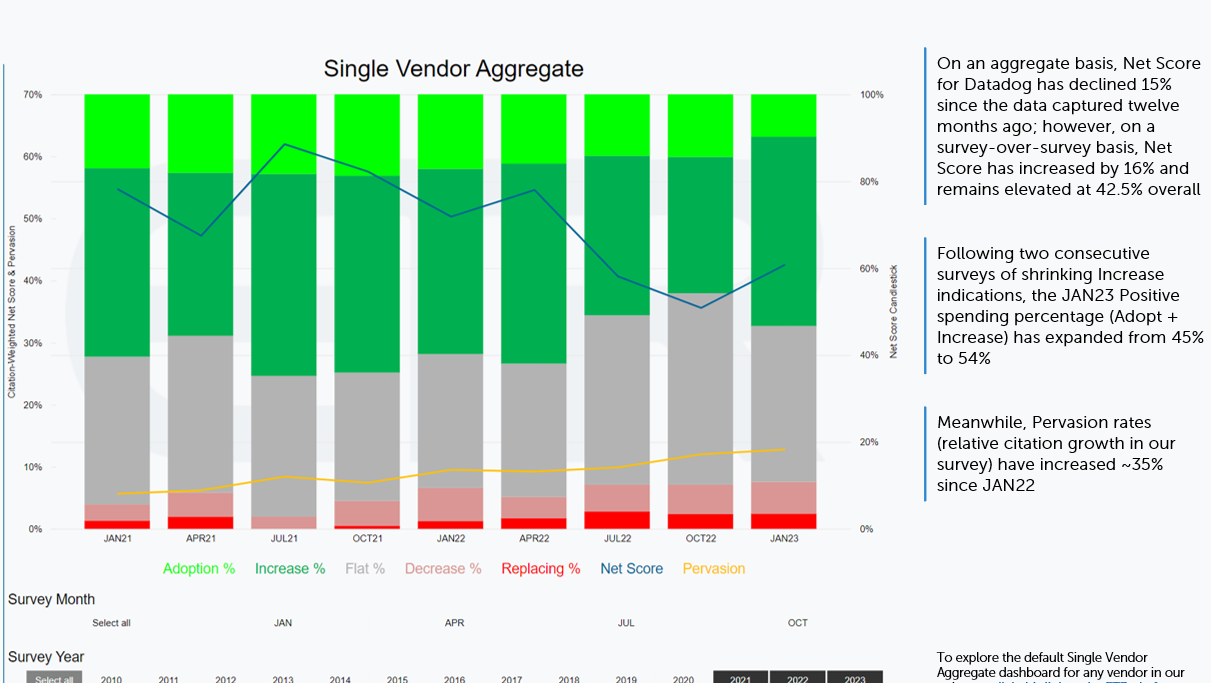

Datadog | ETR Data Outlook: Positive | Earnings Date: 2/16/2023. Back in the OCT22 Datadog report, the ETR research team urged patience, writing, “Amidst broad budget declines, Datadog is inarguably seeing reduced spend intent in our current data set; however, with the drop in Net Score primarily driven by a conservative shift to Flat spend indications, we cautiously retain the Positive outlook on Datadog’s dataset while acknowledging potential changes dependent on the JAN23 spending intentions data.” That patience was rewarded because in this survey period, Flat spending reduced from 44% to 36%, shifting Increase indications materially higher from 31% to 44%.

Moving forward to the most recent Datadog report published last month, the ETR research team stated, "While acknowledging concern over longer-term declines amidst a broader backdrop of declining IT budgets, Datadog’s material survey-over-survey rebounds in sector Net Scores, along with steady Pervasion growth and improved competitive positioning within the Observability peer group, firmly reiterates the Positive outlook on the vendor’s data set heading into 2023."

On an aggregate basis, Net Score for Datadog has declined 15% since that data captured twelve months ago; however, on a survey-over-survey basis, Net Score has increased by 16% and remains elevated at 42.5% overall. Following two consecutive surveys of shrinking Increase indications, the JAN23 Positive spending percentage (Adopt + Increase) has now expanded from 45% to 54%. (see data illustration below)

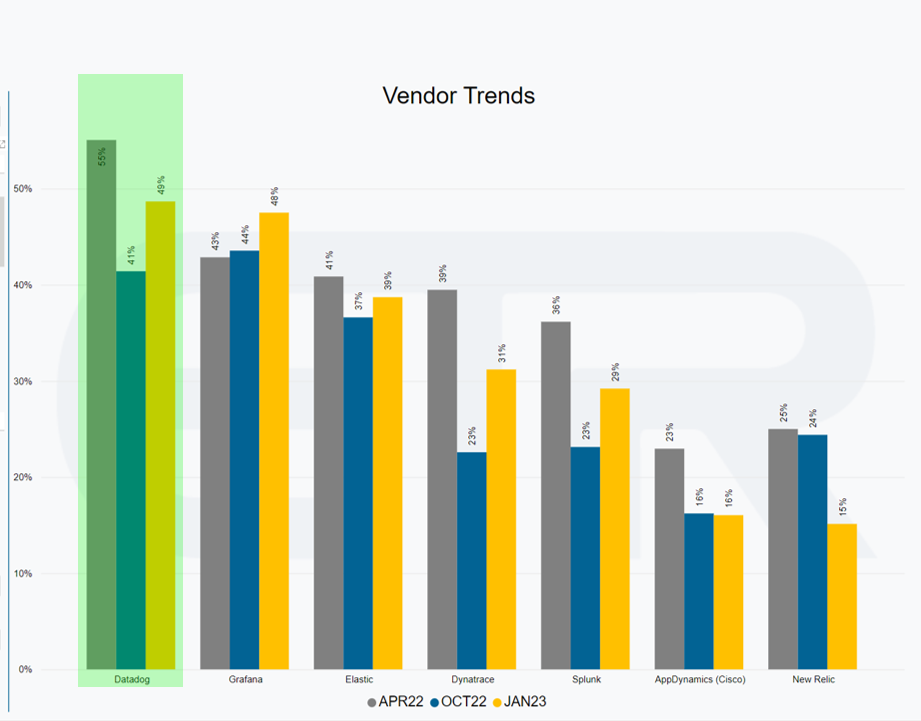

From a competitive positioning standpoint, it should be noted that Datadog leads all of its Observability peers in overall Net Score within the Analytics/Big Data sector (shown below). In addition, the vendor also leads all of its Observabillity peers within the Information Security as well. Relative to its closest comps, this dog is still the leader of the pack.

Lastly, from an equity perspective, shares of Datadog have been buoyed by the recent updraft in tech stocks, rising more than 20% from the low-$60s share price recently seen but still well off peak highs that approached the $200 level back in November of 2021. At current levels, the equity is valued above 60x forward earnings and north of 10x forward sales with strong revenue growth expectations still above 50-60%, according to sell-side analysts, a group that still overwhelmingly support the stock with almost 30 buy ratings versus six hold and zero sell ratings. We shall see next Thursday if those revenue expectations are warranted, but in looking at the spending intentions of Datadog customers in our survey, the reason for optimism is supported by the most recent data set.

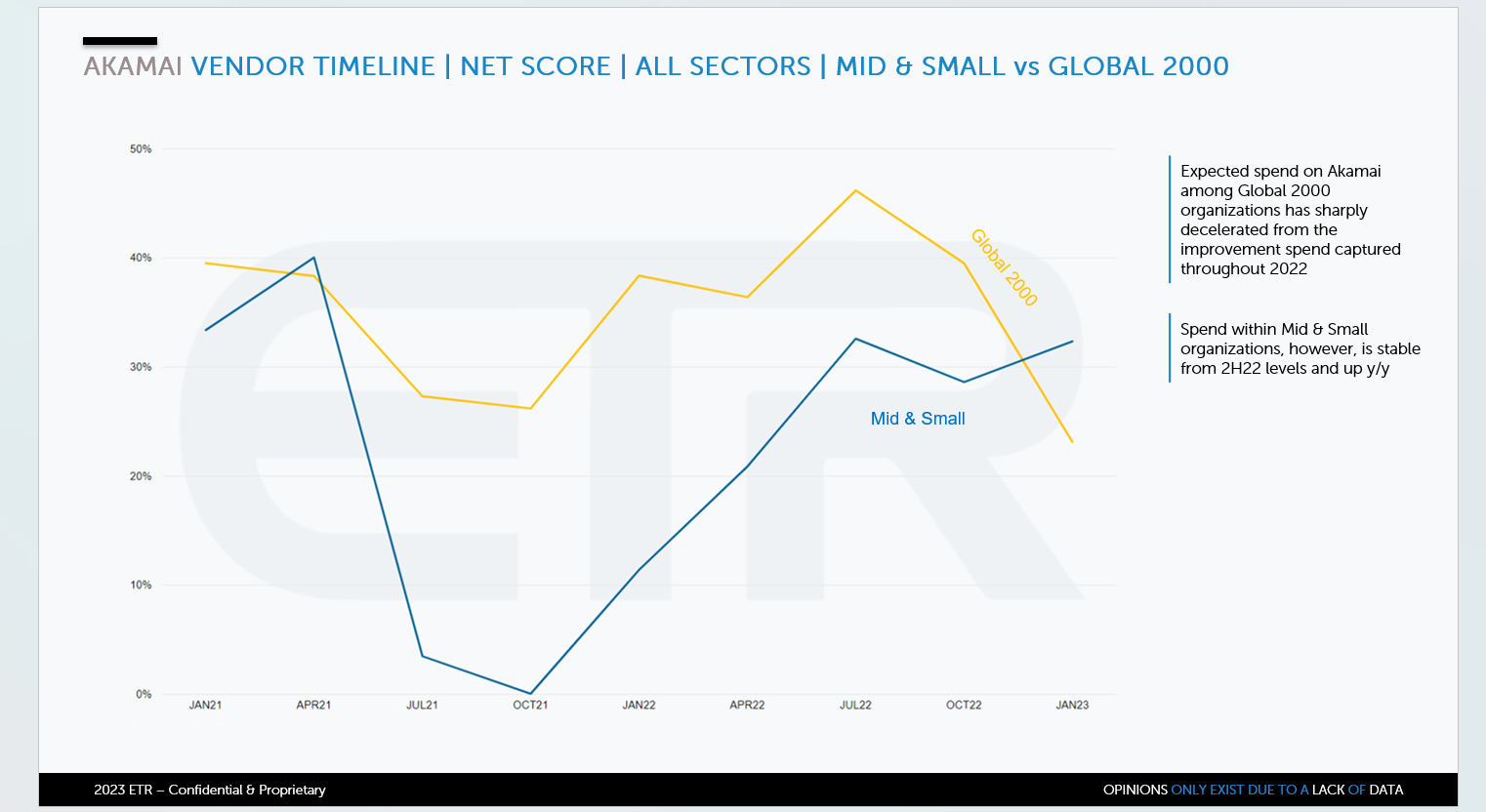

Akamai | ETR Data Outlook: Neutral | Earnings Date: 2/14/2023. Next up, we look at a vendor that lost its Positive data outlook in the most recent report. Akamai was a standout in ETR's 2H22 spending data, with improving spend seen in both Information Security and Networking (CDN), in contrast to broader survey and sector declines, leading us to elevate the company to a Positive viewpoint. While some of that might spill over into the early part of 2023, the divergences in new full-year data between customer types are too large to ignore, leading us to step back to Neutral. After a careful review of the most recent spending intentions data, the ETR team surmised, "while Akamai's 2022 data ended on a high note, mixed full-year data with strength in Mid & Small organizations offset by decelerating spend among larger organizations paints a mixed picture and supports our move back to Neutral."

Akamai's underlying valuation reflects a mature company with low growth expectations trading at forward earnings of 15x, 4x sales, and an attractive free cash flow yield at nearly 8% based on dismal revenue growth estimates mired in the low single-digit range. Given the muted expectations from the sell side and the mixed spending data ETR has captured, it will be interesting to see if there is any love left for Akamai when they report on Valentine's Day.

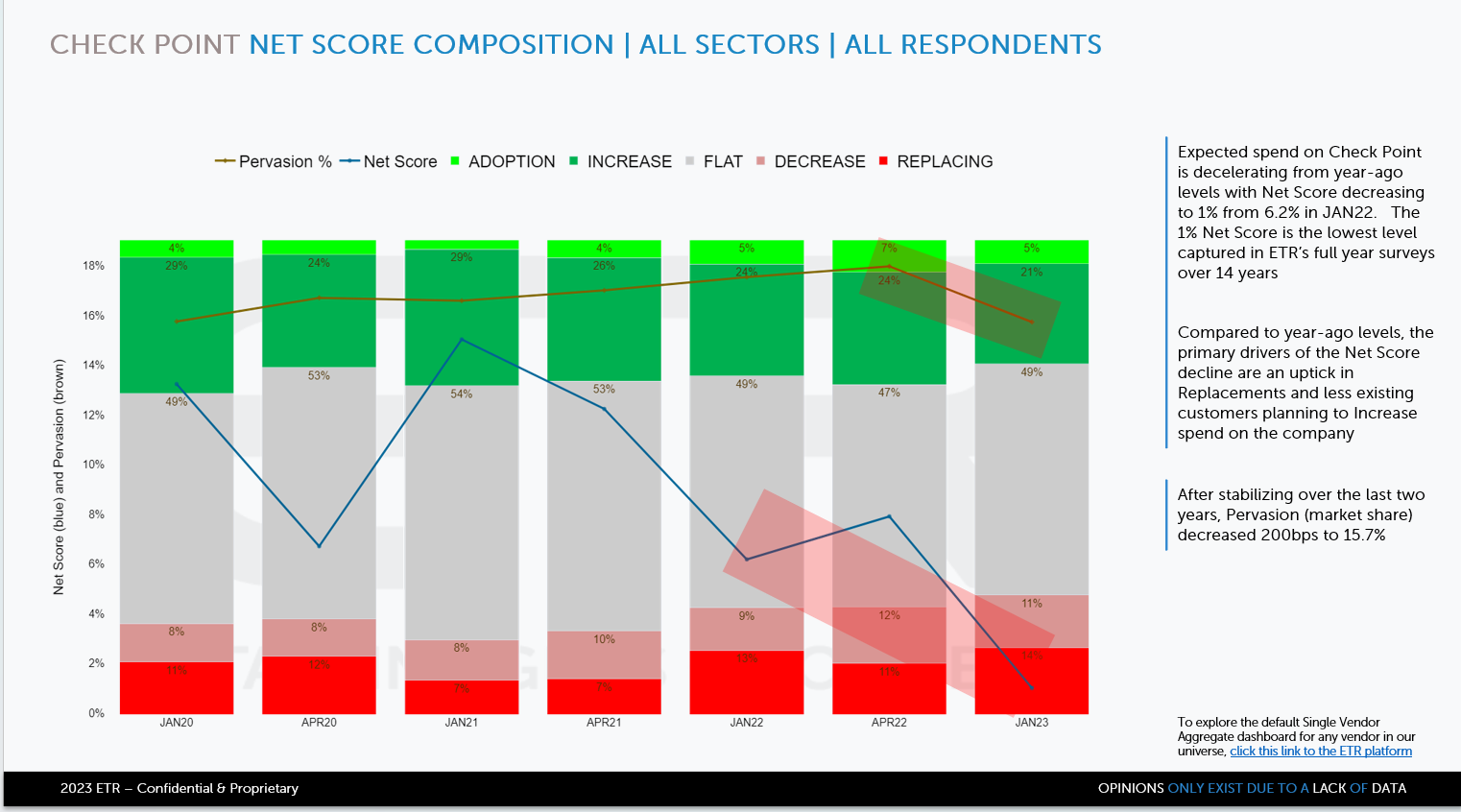

Check Point | ETR Data Outlook: Negative | Earnings Date: 2/13/2023. With Check Point, it's deja vu all over again with another mature legacy vendor with very low growth expectations trading at mid-teens forward earnings multiples and high FCF yields nearing 8%. However, from a data set perspective, Check Point's most recent data is not nearly as well positioned as Akamai. In fact, spending intentions for Check Point in the JAN23 TSIS dropped from year-ago levels to a 1% Net Score (vs. 6.2% Y/Y) and the lowest level captured in 14 years of ETR’s full-year spending intentions surveys. The primary drag on spend is an uptick and continued high level of replacements while plans to increase spend among existing customers has declined. Last year, Check Point was one of a few vendors to see accelerating revenue growth; however, based on forward-looking spending data, continued elevated negativity and weakening competitive positioning does not bode well for a repeat in 2023.

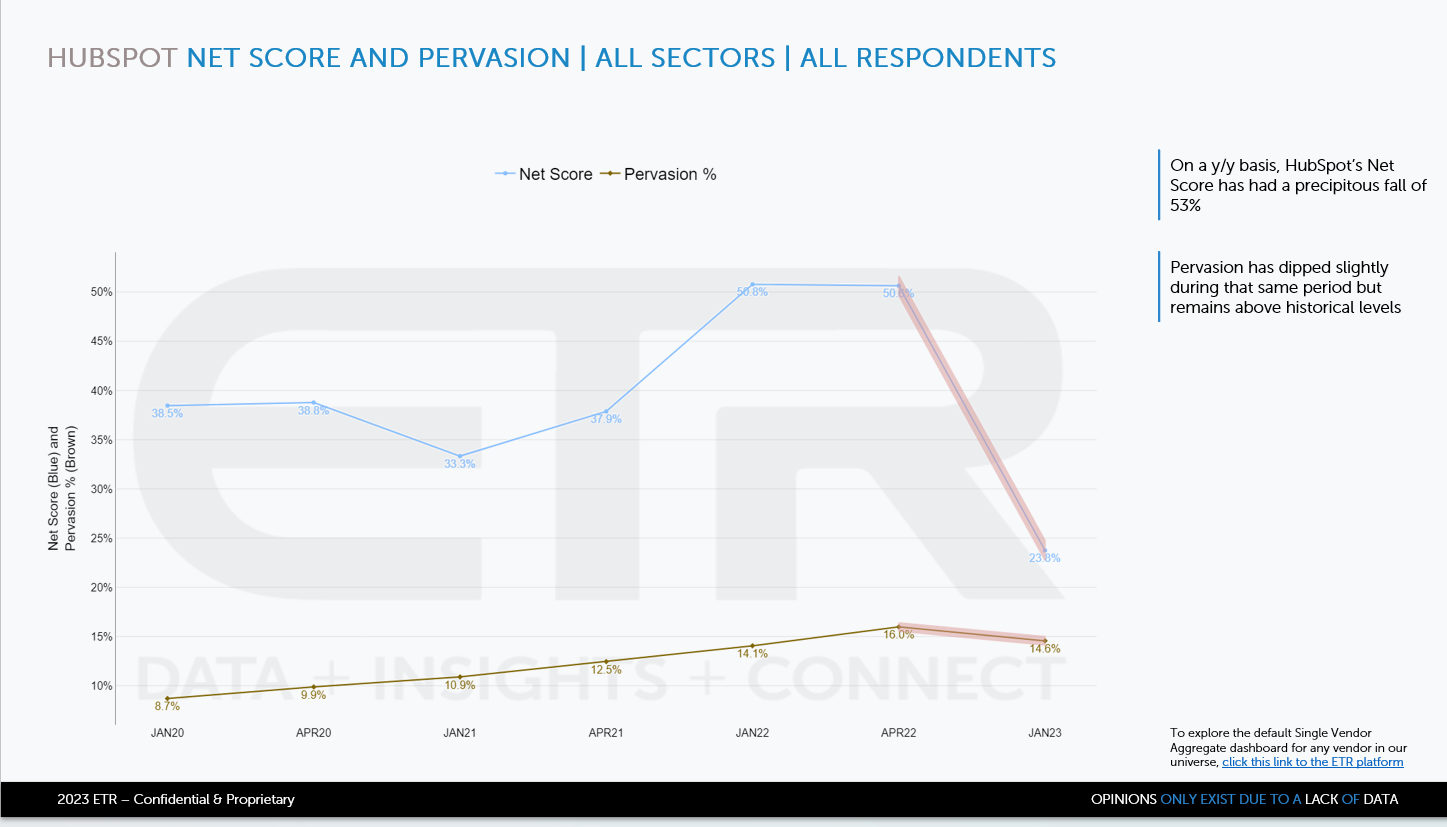

HubSpot | ETR Data Outlook: Negative | Earnings Date: 2/16/2023. Last up for this week is a vendor that maintained a negative data outlook in the most recent survey period, where HubSpot’s Net Score has dropped precipitously year-over-year by 53% as Pervasion also ticks down. Compared to APR22, expected Adoptions for HubSpot have nearly halved, while new churn indications have also entered the dataset. In addition, an increasing proportion of HubSpot respondents indicate flattening spending expectations with the vendor.

Despite aggregate sequential improvements compared to a very poor OCT22 data set, HubSpot fails to capture its previous momentum within the Marketing sector. This, along with three survey iterations where its performance within the Enterprise Apps sector proves lackluster, we are left again with a Negative outlook on HubSpot data.

On an equity basis, the Street has a heavy hand of Buy Ratings with a sprinkling of Hold and, again, zero Sell ratings that this writer could find as of press time. This optimism is paired with rich valuations of well over 100x forward earnings and 8x sales for revenue growth expectations of ~20% for next year. The company is slated to report next Thursday after the market close.

And that's all for this week, folks, but don't fret we will be back in next week's newsletter with some data previews on more ETR-covered vendors like Zscaler, Elastic, and Workday. If you don't feel like waiting around or have the desire to see the full data sets on all of the companies ETR tracks, hop into our leading research platform, or kick off your own free trial to gain access.

Enterprise Technology Research (ETR) is a technology market research firm that leverages proprietary data from our targeted IT decision maker (ITDM) community to provide actionable insights about spending intentions and industry trends. Since 2010, we have worked diligently at achieving one goal: eliminating the need for opinions in enterprise research, which are often formed from incomplete, biased, and statistically insignificant data. Our community of ITDMs represents $1+ trillion in annual IT spend and is positioned to provide best-in-class customer/evaluator perspectives. ETR’s proprietary data and insights from this community empower institutional investors, technology companies, and ITDMs to navigate the complex enterprise technology landscape amid an expanding marketplace. Discover what ETR can do for you at www.etr.ai